By Laura Cassiday

April 2017

- Patterns of edible oil consumption in China have changed with increased urbanization, improved standards of living, and food safety concerns.

- China is now the world’s largest consumer, the second-largest producer, and the second-largest importer of edible oils.

- Soybean, rapeseed, palm, and peanut oils are the most commonly consumed edible oils in China, although “Western” oils and fats such as olive oil and butter are gaining in popularity.

When Keshun Liu was a child growing up in China, he remembers that his mother used pork lard and locally crushed, unrefined rapeseed oil for cooking. “Lard and locally produced rapeseed oil were used interchangeably in family cooking,” says Liu, now a research chemist at the US Department of Agriculture–Agricultural Research Services (USDA–ARS) in Aberdeen, Idaho. “Most families would buy pork, render the fat portion into lard, and use the lard for cooking purposes.” Especially in rural areas, if vegetable oil was available at all, it was typically unrefined and unpackaged. However, this situation has changed drastically in a relatively short period of time. “For years now, people do not eat lard anymore,” says Liu. “They eat refined and packaged vegetable oil, purchased from the grocery store, which is considered a healthier oil.” Many factors have contributed to this shift in cooking oil preferences, including increased urbanization, improved standards of living, and concerns about food safety. And while much of China is becoming increasingly westernized, cultural and economic factors make China’s patterns of edible oil production and consumption unique.

Patterns of consumption

China’s growing economy and rising incomes led to a 440% increase in per capita vegetable oil consumption in China between 1979 and 1999 (Fang, C., and Beghin, J. C., https://dx.doi.org/10.1006/jcec.2002.1796, 2002). By 1999, China was the world’s largest importer of soybean, rapeseed (canola), and palm oils. In 2002, household survey data from 18 Chinese provinces revealed three major regions of vegetable oil consumption (Fang, C., and Beghin, J. C., https://dx.doi.org/10.1006/jcec.2002.1796). Each region had a “staple” vegetable oil that comprised about 80% of total edible oil consumption, with limited consumption of other oils and fats.

In the Northeast region, which consists of the provinces of Heilongjiang, Jilin, and Liaoning (Fig. 1), the staple oil was soybean oil. Rapeseed oil predominated in the Middle and West regions (Jiangsu, Zhejiang, Anhui, Jiangxi, Hunan, Sichuan, Guizhou, Yunnan, Shaanxi, Gansu, Qinghai, and Xinjiang). In the South region, which includes Guangdong, Fuijang, and Guangxi, peanut oil was the most popular. These regional patterns of vegetable oil consumption may be explained by varied climates, land conditions, oilseed production, cultures, and socioeconomic standards. However, as per capita income increases, the pattern of vegetable oil consumption typically diversifies (Fang, C., and Beghin, J. C., https://dx.doi.org/10.1006/jcec.2002.1796, 2002).

FIG. 1. The provinces of China. Credit: Shutterstock

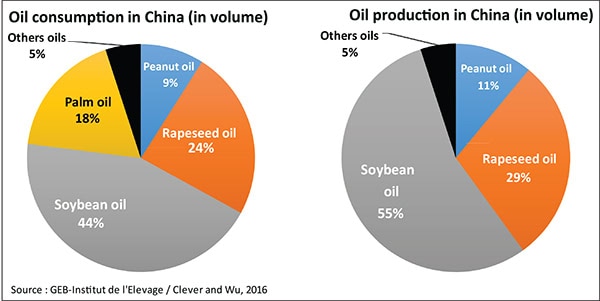

“China is the world’s largest consumer of vegetable oils,” says Yuanfa Liu, professor of food science at Jiangnan University, in Wuxi, China. “With the constant development of the economy and the increase of total population, the consumption of vegetables oils is increasing year by year.” Currently, the top vegetable oils consumed in China as a whole are soybean oil (44%), rapeseed oil (24%), palm oil (18%), and peanut oil (9%), with other oils (cottonseed, sunflower, sesame, camellia, olive, etc.) making up the remaining 5% (Fig. 2, left) (Jamet, J.-P., and Chaumet, J.-M., https://dx.doi.org/10.1051/ocl/2016044, 2016). Consumers are increasingly accepting “Western” oils and fats, such as olive oil, butter, and margarine. The consumption of palm oil, imported from Malaysia and Indonesia, in China has risen considerably in recent years because it is less expensive than soybean or rapeseed oil and has broad applications in processed foods and fried snacks. Soybean oil, rapeseed oil, and peanut oil are produced domestically in China (Fig. 2, right). As for oilseed production in China, peanut predominates (32%), followed by rapeseed (28%), soybean (23%), sunflower (5%), and other oilseeds (12%).

FIG. 2. Vegetable oil consumption and production in China. Credit: Jamet, J.-P., and Chaumet, J.-M. (2016) “Soybean in China: adapting to the liberalization.” OCL 23, D604. https://dx.doi.org/10.1051/ocl/2016044

Rising imports

In recent years, increasing liberalization of China’s economy has affected the edible oil industry. Rationing of vegetable oils in China ended in 1993, and since then the market has been driven by competitive forces (Fang, C., and Beghin, J. C., https://dx.doi.org/10.1006/jcec.2002.1796, 2002). Until 2006, the Chinese government imposed tariff rate quotas (TRQ) on vegetable oil imports to protect domestic products. Quantities of imported edible oils below a specific quota were taxed at one rate (for example, 13%), whereas imports above the quota were subject to a substantially higher tariff (for example, 90%). With accession to the World Trade Organization, China phased out the TRQ for soybean and rapeseed oil, leaving only a 9% import tariff for soybean oil and rapeseed oil imports. TRQ on sunflower, peanut, and corn oil were also eliminated and replaced with a 10% tariff.

A growing population combined with free-market forces have brought about dramatic changes in agricultural trade in China. Until the mid-twentieth century, China was self-sufficient in feeding its population (Jamet, J.-P., and Chaumet, J.-M., https://dx.doi.org/10.1051/ocl/2016044, 2016). However, in the 1960s China began to import cereals, especially wheat, as Chinese agriculture was unable to keep up with demand. Since the 1990s, China has experienced steady economic growth and an increased standard of living, which has caused the economy to move even further away from self-sufficiency.

Until the 1950s, China was the world’s largest soybean producer, and the country remained a net soybean exporter until the 1990s (Jamet, J.-P., and Chaumet, J.-M., https://dx.doi.org/10.1051/ocl/2016044, 2016). In the past, most soy in China was used for human consumption in foods such as tofu, soy sauce, miso, and tempeh. In recent years, increased soybean oil consumption, as well as an increased demand for animal feed (and thus soymeal) to support China’s growing livestock industry, have greatly affected the soybean market. With higher incomes and increased westernization, Chinese households are now consuming more meat and dairy products than ever before, increasing the demand for livestock feed and soybean meal. China has been forced to increase soybean imports to keep up with the demand.

Because arable land in China is limited, the Chinese government made the strategic decision to achieve and maintain independence in cereals at the expense of other crops, such as soybeans (Jamet, J.-P., and Chaumet, J.-M., https://dx.doi.org/10.1051/ocl/2016044, 2016). In particular, corn production has doubled in the past 15 years, supplanting soybean cultivation in many areas. Whole, unprocessed soybeans are imported for domestic processing. In 1999, the tariff on whole soybean imports was lowered from 180% to 3%. Unlike soybeans, TRQ remain for rice, wheat, and corn, encouraging domestic production. However, even with these challenges, China remains the fourth largest soybean producer in the world.

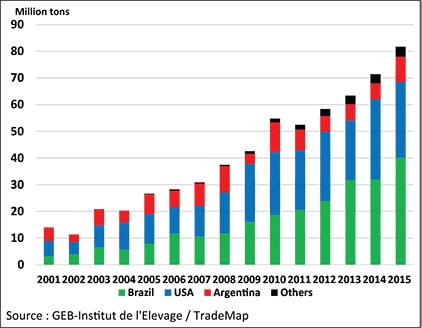

China is the world’s largest importer of soybeans, with 63.5% of the import share in 2013 (Yang, T. K., and Zheng, Y., Inform 27, 24–25, 40, 2016). Most soybeans are imported into China from Brazil (49%), the United States, (35%), and Argentina (12%) (Fig. 3). Seventy-five percent of Brazil’s, 50% of the United States’, and 85% of Argentina’s soybean exports are sold to China (Jamet, J.-P., and Chaumet, J.-M., https://dx.doi.org/10.1051/ocl/2016044, 2016). Most rapeseed oil in China is produced from domestic seed, with rapeseed and rapeseed oil imports coming primarily from Canada.

FIG. 3. Chinese soybean imports. Credit: Jamet, J.-P., and Chaumet, J.-M. (2016) “Soybean in China: adapting to the liberalization.” OCL 23, D604. https://dx.doi.org/10.1051/ocl/2016044

To assist soybean farmers with rising production costs, in 2008 the Chinese government set a minimum price for domestically produced soybeans (Jamet, J.-P., and Chaumet, J.-M., https://dx.doi.org/10.1051/ocl/2016044, 2016). As a result, the price of domestic soybeans in China is significantly higher than that of imported beans. In 2013, the price of imported soybeans averaged USD $600 per ton (plus a 3% tariff), compared with a price of USD $750 for domestically produced soybeans. Thus, many Chinese seed crushers have favored imported soybeans over domestic.

To make domestic soybean prices more competitive, in 2014 the Chinese government changed the soybean and rapeseed subsidy system. Now, instead of guaranteeing a minimum price, the system sets a “target price” and provides a “deficiency payment” for the difference between the target price and the market price. Because of the new system, between January 2014 and December 2015 the price of Chinese soybeans fell by 20%, but soybean imports still did not slow due to increased demand for animal feed and oil.

China’s “Crops structural adjustment plan 2020” aims to reduce the production of corn and encourage farmers to increase planting of peanuts, soybeans, alfalfa, and other crops (Jamet, J.-P., and Chaumet, J.-M., https://dx.doi.org/10.1051/ocl/2016044, 2016). The plan calls for reducing areas planted with corn by 3.3 million hectares, going back to the 2011 level. In contrast, the soybean surface area will be increased by 2.6 million hectares, restoring the 2006 level. Although these measures will boost domestic soybean production, the need for imported soybeans will likely continue.

China’s soybean-crushing industry

The soybean production areas in China are primarily located in the northeast and central east provinces. Prior to the 1990s, soybean-crushing plants were mostly locally owned and situated in the producing areas. With increasing soybean imports, many new crushing plants were built along the coastal region (Jamet, J.-P., and Chaumet, J.-M., https://dx.doi.org/10.1051/ocl/2016044, 2016). Because of the lower price of imported soybeans and barriers to transportation for domestic soybeans, it became less expensive for crushing facilities near harbors to purchase imported soybeans.

The large volume of soybean seeds crushed in China (70 million metric tons in 2015) has made the country self-sufficient in soybean meal, and China is a net exporter of soymeal to countries such as Japan, Vietnam, and South Korea (Jamet, J.-P., and Chaumet, J.-M., https://dx.doi.org/10.1051/ocl/2016044, 2016). However, China remains a net importer of soybean oil. Although China’s capacity for edible oil refining has increased dramatically in recent years, and China is the world’s largest soybean oil producer, the demand for soybean oil has risen even more rapidly.

Since 2005, the majority of China’s soybean-crushing industry has been owned by foreign companies (Jamet, J.-P., and Chaumet, J.-M., https://dx.doi.org/10.1051/ocl/2016044, 2016). In April 2004, when soybean prices were at a peak, Chinese crushers agreed to buy US soybeans. Six months later, when the payments were due, soybean prices fell dramatically. Many soybean buyers tried to default on their contracts, but an international court ruled against them. The “2004 soybean crisis” resulted in huge monetary losses and the bankruptcy of many Chinese crushing companies. Consequently, many international companies built or purchased crushing facilities in China. Currently, about 60% of China’s soybean crushing is performed by international companies such as ADM/Wilmar, Bunge, and Cargill.

Changing times

Under China’s thirteenth Five-Year Plan (a government blueprint for social and economic policies for the years 2016–2020), China’s oil processing technology and manufacturing equipment will expand in scale and become increasingly automated, intelligent, and energy-efficient, says Xuebing Xu from Wilmar Global R&D Center, in Shanghai, China. “China is one of the world’s largest edible oil-producing, -consuming, and –importing countries,” he says. “China’s oil research and oil processing technology, as well as the apparatus, are reaching an internationally advanced level.”

In the past, most vegetable oil in China was bought in bulk and suffered from quality and safety issues. “In recent years, the Chinese government has increased its emphasis on food safety,” says Ruiyuan Wang from the Chinese Cereals and Oils Association, in Beijing. “Government and industry are working together to reduce unhealthful oil components.” In 2011, some large Chinese cities such as Beijing and Shanghai banned the retail sale of bulk edible oils. Higher-quality, refined oils in smaller packages are becoming increasingly common throughout China.

This increased focus on food safety includes enhanced surveillance and penalties for the production and sale of gutter oil—used cooking oil that is illegally collected from restaurant waste and gutters, crudely processed, and sold as a cheaper alternative to new cooking oil. Gutter oil, which has been a major problem in China, Taiwan, Hong Kong, and other countries, often contains toxins and carcinogens that are harmful to human health.

“With the constant development of the economy, increasing income of residents, as well as increased urbanization of China, people are more concerned with the safety and nutrition of food and with a healthy diet,” says Yuanfa Liu. Edible oils perceived as healthful, including camellia, sunflower, olive, rice bran, and corn oils, are growing in popularity.

However, the Chinese people may not be ready to accept genetically modified (GM) vegetable oils with beneficial fatty acid profiles, such as high-oleic soybean oil. Surveys indicate that the vast majority of the Chinese public is wary of GM crops. The government has officially banned GM commercial crops, and currently only non-GM soybeans are grown in China. More than 60% of these domestic, non-GM soybeans are used in foods such as tofu and soy milk (Jamet, J.-P., and Chaumet, J.-M., https://dx.doi.org/10.1051/ocl/2016044, 2016). Imported GM soybeans are allowed for the production of edible oils and animal feed, but not for food use. Most GM soybeans have a 3–5% higher oil content than non-GM soybeans, as well as lower production costs.

Recently, the Chinese government has indicated an increased willingness to explore GM technology in order to improve domestic crop productivity. “With time and the popularization of GM scientific knowledge, GM vegetable oils rich in beneficial fatty acids will gradually be accepted by consumers,” Xu predicts.

Despite the fact that China is becoming increasingly westernized, patterns of edible oil consumption in China still differ substantially from those in North America and Europe. “In the West, we use a lot of butter, margarine, and shortenings in breads and bakery products,” says Keshun Liu. “But in China, bakery products are not very common. We normally eat a steamed bread, which does not include shortening as an ingredient.” He notes that most modern Chinese kitchens do not contain ovens because baking a cake or bread at home is so uncommon. “The Chinese are going to westernize, but they will still keep their own traditions,” says Liu. “Even though some people in the urban population like butter or margarine, and others like French fries, pizza, or fried chicken, the majority of people in the rural areas cannot afford or have access to western food.”

Laura Cassiday is an associate editor of INFORM at AOCS. She can be contacted at laura.cassiday@aocs.org.

INFORMation

- Fang, C., and Beghin, J. C. (2002) “Urban demand for edible oils and fats in China: evidence from household survey data.” J. Comp. Econ. 30, 732–753. https://dx.doi.org/10.1006/jcec.2002.1796

- Jamet, J.-P., and Chaumet, J.-M. (2016) “Soybean in China: adapting to the liberalization.” OCL 23, D604. https://dx.doi.org/10.1051/ocl/2016044

- Yang, T. K., and Zheng, Y. (2016) “Chinese edible oils market and consumption trends.” Inform 27, 24–25, 40. (February 2016)

Hot Topic: China’s fat and oil industry

Do you want to learn more about edible oils and fats in China? Then make plans to attend the Hot Topic session, “China’s fat and oil industry: a fast-growing segment with opportunities and challenges” at the 2017 AOCS Annual Meeting and Industry Showcases April 30–May 3 in Orlando, Florida, USA.

The session, sponsored by the newly established China Section of AOCS, will provide timely updates on the current status of the fats and oils industry in China, including production, consumer trends, research and product development, and markets for edible oils as well as protein co-products. Invited speakers are industry leaders and top scientists in China.