Short- and long-term price forecasting for palm and lauric oils

By Dorab E. Mistry

February 2011

Note: The following paper represents excerpts from a talk delivered by Dorab E. Mistry at the 6th Indonesian Palm Oil Conference (IPOC) & 2011 Price Outlook, organized by the Indonesian Palm Oil Association (GAPKI) and held December 1–3, 2010, at the Westin Resort Nusa Dua, Bali.

Ladies and gentlemen:

The year 2010 has been a very happy one for the palm oil industry. The GAPKI conference is well timed and for me personally, some of my most successful forecasts happen to be made at GAPKI conferences. At this conference in December 2009, I forecast that growth of crude palm oil (CPO) production in Indonesia would be curtailed in 2010 by the developing El Niño, occurring at the same time as the low turn of the biological cycle, despite a rise in mature acreage. This combination of events would also push Malaysian production into negative territory. As a result I gave a bullish prognosis for 2010.

At the Palm and Lauric Oils Conference & Exhibition (POC) held in Kuala Lumpur in March 2010, I forecast 2010 Malaysian production at just 17.2 million metric tons (MMT) and Indonesian production to grow by only 1.5 MMT. I also forecast CPO prices to exceed 3,000 ringgits ($1,000) per metric ton in the second half of the year.

I also forecast a decline in the US dollar starting July 1, 2010. All three of my forecasts have come true. The CPO production model that I have developed and refined over my 30 years in this industry has performed extremely well this year.

Measures taken by China

As we all know, the Chinese government has become very concerned at domestic inflation and announced several measures to tackle it. The Chinese government has over the years displayed remarkable foresight and determination, and therefore its actions have earned the respect of the market.

To my mind, a wise and astute government has four basic measures to undertake when it wishes to clamp down on domestic inflation:

1. Curb and wipe out local speculation, black marketing, and profiteering.

2. Tighten money supply and remove or rein in excess liquidity in the local market. Excess liquidity leads to speculation and hoarding.

3. Allow the exchange rate to rise, or raise interest rates to control money supply and liquidity.

4. Most importantly, raise the supply of goods and commodities in the local market.

The fourth measure is the best and most potent weapon that government has. Supply can be increased by releasing State Reserve Stocks or by undertaking large imports. An increase in supply can be made more effective by subsidizing imports, by removing import taxes, or by the government's importing these commodities and selling them at a loss. All these measures are very effective and will lower inflation very quickly. Subsidies may be wasteful, but for a short period they can be very effective. The Chinese government also has one other useful weapon. In 2009, it bought a large stock of domestic rapeseed oil as a price support measure. It can now release that stock to increase supply at reasonable prices.

There is a fifth measure, price control, which is usually effective in the very short term but is very damaging in the long run. This measure will lower prices for a few weeks, but it will damage producers, lower future production, and consign the country to shortages. It is not a market-based solution and must be avoided at all costs. People and producers are not stupid. They will stop producing if they have to incur losses. People will consume more and hoard if they find prices artificially low.

The government of China is wisely undertaking the first four of the five measures I have outlined. The first three have a mildly bearish effect on world prices. The fourth measure, of increasing supply and undertaking large imports, will have a positive impact on world prices. So on balance, the effect of all four measures on world prices should be neither positive nor negative in the medium term.

Prices will be made by fundamentals of supply and demand plus external factors such as worldwide investment funds and exchange rates.

My conclusion is that the Chinese government's measures should not be viewed as bearish or bullish except in the very short term. It takes the market a few weeks to absorb the shock and for the fundamentals to re-assert themselves.

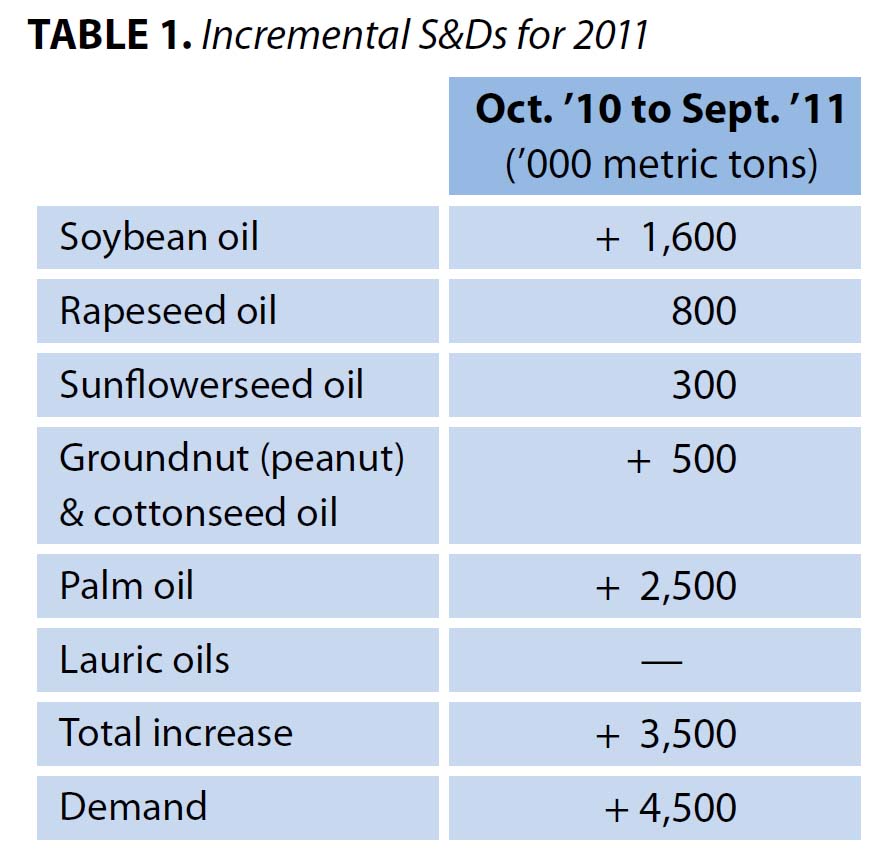

With those remarks on the immediate worry of the market, I shall speak on the Incremental S&Ds for the oil year October 2010 to September 2011.

Incremental S&Ds for 2010-2011

In both 2008-2009 and 2009-2010, Incremental Demand outstripped Incremental Supply and we had to draw down stocks. Let us see if we have to draw down stocks further for the third year in succession.

Palm: As I have been explaining over the last 12 months, the biological low cycle will run from September 2010 until at least March-April 2011. Hence CPO production in the first quarter of 2011 will continue to underperform, and stocks will continue to be drawn down. Supply will be most critical and tight during this period. We can expect a recovery to begin from April 2011, but this recovery will be neither as strong nor as impressive as previous ones. As time goes by and I have more data in hand, I shall expand on this in my paper at POC in Kuala Lumpur March 8-9, 2011.

Last year as we were experiencing an El Niño, the signals of a pending shortfall in production were very strong. This year has been more nearly normal, and therefore the signals are not as strong. If last year my production forecast was made with a 90% confidence level (that is why I never changed my forecast despite universal disagreement), this year the confidence level is lower, at about 75%.

My prognosis for the 2011 calendar year is for Malaysian production to recover by 500,000 MT and for Indonesian production to recover by 2 MMT. Most of this recovery will be seen in the second half of 2011 and will spill over into 2012.

Generally the recovery after an El Niño year is fueled by two powerful engines-higher fertilizer application during the period of high prices, which kicks in during the later part of the production decline, and the new acreage that begins to produce once rainfall improves.

This time around, the extra kick provided by accelerated fertilizer use will not be so strong because too much fertilizer has already been applied, thanks to very high CPO prices throughout 2010. In fact we may see the law of diminishing returns come true! Acreage expansion has also slowed dramatically owing to the activities of NGOs (nongovernmental organizations) and the regulations enacted by the Indonesian government.

Soybeans: The world is anxiously watching the current growing season in South America. La Niña is in force, but we have to see if it results in dry weather and how much that impacts soybean yields. Currently, world S&Ds are based on a crop of 67 MMT in Brazil and 52 MMT in Argentina. Yet the S&Ds are very tight. If we lose a few million metric tons, the soybean S&Ds will get to rationing levels. We shall then have to rely on a big expansion in acreage in the United States in 2011 plus almost ideal growing weather.

For the present, the world is also focused on Chinese monthly imports of beans. If the Chinese government releases State Reserves and skips one month's imports, these actions will have a bearish impact on prices in the short term. The recent downswing in prices has already perhaps taken that into account. If, on the other hand, Chinese monthly bean imports remain at their level of the past few months, prices will quickly recover and resume their upward march. For world prices to be driven down and kept down, the Chinese government has to demonstrate convincingly that estimates of Chinese bean imports are exaggerated by 3-4 MMT and that they can skip one month's imports without replacement.

So the fate of prices in the short term rests on Chinese import demand and on South American weather.

I must draw your attention to the fact that the current La Niña is one of the strongest in recent decades. It must affect crops in South America. The present indications are that we shall lose at least 5 MMT of soybeans as compared to earlier crop expectations. We cannot be complacent on this score. Most analysts underestimated the effects of the 2009 El Niño and appear to be doing the same with this La Niña.

In this day and age, we are making our farms and plantations perform almost to perfection. By piling on fertilizers and growth promoters, we have pushed yields to extremely high levels, depending on growing conditions to be almost ideal. Any disturbance by drought or flood leads to a disproportionate effect on yields. I invite you to imagine an old truck that is being run around the clock. It will run well on good roads in good conditions, but give it some rough terrain and it will break down. As world climate gets more capricious, world agriculture will fail to keep producing record high yields. And we have come to rely on super-high yields. I have already lopped 5 MMT from current South America soybean crops, and I stand ready to reduce estimates further as the season progresses.

And after the harvest, we shall have to crush an additional 8-10 MMT of beans to find the extra soybean oil required by the world.

Rapeseed: Production numbers for rapeseed have improved slightly in the last few weeks, and prospects for the Indian crop are distinctly brighter. I am therefore reducing the shortfall in rapeseed oil production this year to 800,000 MT from my earlier estimate of 1 MMT.

Sunflowerseed: Prospects for sunflowerseed production have also improved in the last few weeks in Ukraine. I am still wary of the Argentine production. Therefore, I am keeping the shortfall in sun oil production at 300,000 MT.

I continue to believe that groundnut oil and cottonseed oil production will increase by about 500,000 MT due to higher crush.

I also continue to believe that coconut oil production will decline and will balance the additional availability of palm kernel oil (PKO).

Demand scenario

It now looks as though the dreaded double dip recession is not going to happen. The calendar year 2010 will end with the world economy growing on average in excess of 4%, with a forecast of even better growth in 2011. Biodiesel mandates in several countries will continue to expand and so will growth in population and in per capita consumption in the developing world. However, we are at very high levels in terms of price, and hence we must estimate growth in world demand to be 4.5-5 MMT only for oil year 2010-2011.

Now we can see the developing Incremental S&Ds for next year (Table 1).

{kind=link}

The US Congress reassembled on November 29 and we must watch its actions on the ethanol subsidy and the Blenders Credit for biodiesel. The implementation of RFS2 (Renewable Fuels Standard 2) also needs to be watched. Even if only one of these three factors comes into play, it will be very bullish for corn, beans, and bean oil.

At present, it looks like for the third year in a row, Incremental Supply will not match Incremental Demand. There is a shortfall of at least 1 MMT.

While palm production will recover, we shall encounter lower production of soybeans and sunflowerseed in South America. Overall, oilseed and oil production will not have a chance to recover strongly.

Price outlook

I expect prices to rise from current levels in the next six months. Any price decline will have to wait until June-July when Northern Hemisphere crop prospects can begin to weigh on the market. My price outlook extends to the next six months. I also expect Inverses to assert themselves because stock levels in the next few months will be extremely tight.

I presume that there will be no unexpected war (North Korea or Iran?), that the US dollar will run out of steam by January 2011, that mineral oil prices will hold at current levels and gradually move higher, that the Euro zone will be stable, and that monetary policy in the United States and Europe will be easy and relaxed.

Palm: My November prognosis for CPO futures on the BMD [Bursa Malaysia Derivatives] to reach 3,300 ringgits was fulfilled within two days of the forecast. These are days of instant gratification. So I have to be extremely careful as to what I say. However, it is better to be forewarned than to be surprised. Too often the market gives out wrong signals. I repeat: The price declines of May and June 2010 were based on wrong production forecasts by overoptimistic pundits. Demand boomed at lower prices, and we now have to ration demand with higher prices.

Based on my production prognosis, the period of greatest tightness will be between February and May 2011, and we need prices to rise now to rein in demand and to stimulate plantings. At some stage in December-January I expect RBD [refined, bleached, deodorized] palm olein to trade at US$1,250 per metric ton FOB with CPO futures on the BMD trading at 3,600 ringgits.

Other oils: Soybean oil prices also need to rise because too much incremental demand from sunflowerseed and rapeseed oil consumers is migrating in its direction. A level of US$1,250-$1,300 FOB Argentina is to be expected.

Sunflowerseed oil will maintain a premium of about US$200 over soybean oil prices.

I expect rapeseed oil prices also to maintain a premium of US$100-$150 over soybean oil.

PKO has already touched US$1,650 CIF (cost, insurance, freight) Rotterdam. Demand for FMCG (fast-moving consumer goods) products in the West as well as the East is very strong, and it is quite possible that PKO prices will go close to an unprecedented level of US$1,800

CIF Rotterdam. The outlook is the same for coconut oil.

What are the threats to this forecast?

The threat of contagion is the most prominent. Equity and bond markets need to be stable and must not fall. Countries such as Ireland, Greece, Portugal, Spain, or Belgium need to keep their house in order. The flow of investment money into commodities must also remain stable.

RSPO

Over the years I have remained a strong supporter of the Roundtable on Sustainable Palm Oil (RSPO). Much progress has been achieved. On the other hand, the uptake of certified sustainable palm oil has been disappointing. Those who talk of sustainability need to put their money where their words are. And finally, it is time for the Executive Board of the RSPO to reflect more proportionately the interests of all stakeholders, not merely in terms of functionality but also in terms of geography. Asia produces 95% of the world's palm oil and consumes 80% of it. Asia has preserved most of its forests, and millions of its people depend on this industry for their livelihood. Yet on the RSPO, Asia is in a minority. Make no mistake. There is no forum other than

RSPO to handle this agenda, but RSPO needs to be reformed. I sincerely hope such reform will be taken up without delay.

Conclusion

I once again congratulate GAPKI on making this conference such an important event on the palm oil calendar. I shall conclude by reminding you of what the Sage of Omaha (Warren Buffett) said once: "Only when the tide goes out do you discover who has been swimming naked." Swimmers need to be aware that the palm oil tide is running out.

Dorab E. Mistry is director, Godrej International Ltd., Mumbai, India. He may be contacted at dorab.mistry@godrejinternational.com.